Kevin O’Leary: You'll Become Wealthy Without the Risk Exposure if You Understand MPT.

Steal this approach that 99% of wealth funds use, or do the opposite.

Authors Remark:

Ahoy there, you magnificent bunch!

Thanks to you, my blog is on steroids and headed to Valhalla.

I'll spare you the "I never thought it'd be possible" etcetera, and dive straight into it.

After doing some back-of-the-takeaway-menu maths, my 296 articles, after slaving behind a computer screen for 18 months, have garnered 1.2 million views.

I’m now looking to take my once small writing passion and make it into a full-time gig, with hopefully the help from you, my most dedicated readers.

Each blog with the background research I put in can take anywhere from 10 to 25 hours.

I’ve decided to only give access to my most prized writing to those who support me for the price of a coffee!

90% of what I write about will remain free forever; however, twice, maybe three times a month, I'll send out a paid newsletter which will delve into deep nuanced research around modern finance topics and current event, without the jargon.

Think of it as the lazy person’s guide to keeping up to speed in bite size snack

Firstly, your support as a subscriber means the world to me.

Secondly, by upgrading to a paid subscription, you'll play a crucial role in helping me achieve writing as a full-time pursuit.

I'm excited to connect with you more, in the meantime, enjoy the piece below.

I wish you a fantastic rest of your Sunday.

Jayden

You did it again, didn’t you?

You built up some savings from your overtime over the last few months and got a juicy end-of-the-month bonus.

Now you’re contemplating what to do with it.

As Ray Dalio says, when you save, you’ll have a different conversation with yourself than the person who spends impulsively.

The next natural question you’ll ask yourself is, where do I keep the money I’ve saved?

You could;

Book another holiday.

Splash out on a new wardrobe.

Make some home improvements.

Keep it in a savings account, earning interest?

None allows you to grow your wealth over time, so you set out to scratch your investing itch.

You’re inexperienced and dive headfirst into an investment with a scattergun approach and your emotions leading the way.

I’ll share one of my investing sins to be a good sport.

It’s what I did when I first bought Facebook stock.

I intuitively thought their ad product was underpriced, which it was.

I assumed that as more advertisers moved away from television and print and used social media advertising, Facebook (Meta) would make increasingly more profit, which they did.

That was it, though.

I had no information on the management team.

No insights into earnings or growth potential.

No understanding of market trends.

No company financials.

No strategy.

I might as well have rolled the dice on a roulette wheel in a rundown casino.

It was beyond risky.

Kevin O’Leary goes by his tongue-in-cheek nickname, Mr. Wonderful.

Following season one of Shark Tank, a would-be entrepreneur tried selling him a music publishing deal; O’Leary proposed an aggressive 51% equity position to control the company, which his co-hosts saw as Militant.

So the name Mr Wonderful was born.

You see O’Leary’s softer nature when he speaks about his late mother, a skilful investor.

Georgette Booklam managed her finances meticulously, but no one knew the level of her success until after her death.

She followed a straightforward strategy, which Kevin says reduces your risk exposure and gives you a shot at wealth.

And the markets will be kinder to you.

Modern Portfolio Theory (MPT)

There’s a growing trend of entrepreneurs who cite their moms as underpinning their success.

O’Leary says the most significant lesson he learned from his mother was the basic portfolio theory of diversification.

He says in her day, there were only ten sectors in the S&P500; today, there are 11, including real estate.

The theory suggests that you should never put more than 20% in one sector and no more than 5% into a single stock.

The strategy “forces you to get diversified, and the market treats you better when you’re diversified because you never know what’s going to happen.”

American economist Harry Markowitz pioneered the theory in his paper “Portfolio Selection,” for which he won a Nobel Prize.

MPT assumes you prefer less risky investments, and with that aversion to risk, it implies you should invest in multiple asset classes to spread the uncertainty.

The expected return is on the entire performance of your diversified portfolio.

The hypothetical figures below show five equally weighted assets, the 20% Kevin’s mom suggested and expected returns of 4,6,9,11 and 15 per cent = 8.5% total portfolio return.

4% gain x 20% invested in a single sector +

6% gain x 20% invested in a single sector +

9% gain x 20% invested in a single sector +

11% gain x 20% invested in a single sector +

15% gain x 20% invested in a single sector +

= 8.5% total portfolio return.

So, if you cut out the above calculations, all it’s saying is to put your investments in several places because you never know what bad luck you’ll have.

Your view on constructing a portfolio may change when you read further.

The Oracle of Omaha Says, “It’s a load of old twaddle.”

Any strategy with the word “theory” will be on the receiving end of criticism.

Warren Buffett is brilliant at identifying the best businesses to buy.

He has a skill that many do not possess.

He’s also firmly in the camp of “concentrators.”

Buffett believes volatility does not equal risk and “you shouldn’t be investing in more than six companies in your lifetime because very few people have ever got rich with their 7th best idea”.

You’ll be making a terrible mistake if you’re searching for a 7th business to invest your money instead of putting more money into your first.

You get more wealthy just doubling down on your first idea.

A good diversifier will always beat a bad concentrator (there’s a caveat)

Picking between concentration and diversification is a hot potato among investors.

If you pursue diversification, it can have a trade-off of greater risk control but less upside — something everyone understands intuitively.

Researchers in Australia ran a study on the Australian stock market and wanted to determine which strategy performed best.

They specifically wanted to compare two approaches, one where fund managers diversified their investments and the other of concentrating much of their money into fewer stocks.

The Aussie researchers looked at how much money each strategy made over time.

They also measured an “information ratio”, similar to a Sharpe ratio, an investment’s risk-adjusted returns. i.e. How much risk vs. reward does this investment give me?

The higher the information ratio, the better the risk-adjusted returns and the better the investment.

The researchers found that concentrated investments in a smaller stock pool outperformed diversification — every time.

Fund managers who invested heavily in a few stocks they hand-picked faired better than when they diversified their investments.

It led to higher profits even when considering the risk factor of potentially more significant losses.

The researchers concluded that there were two significant factors in the success of concentrated investing.

It was the joint impact of these two decisions.

Stock selection

Portfolio construction

In other words, could you pick the right stocks?

And then, could you combine your small group of stocks to form an investment portfolio, weighing the right amount of money in each to maximise your profits?

When I was greener than an Amazon rainforest putting my hard-earned mullah into Facebook stock, I’m not sure I could’ve got this right.

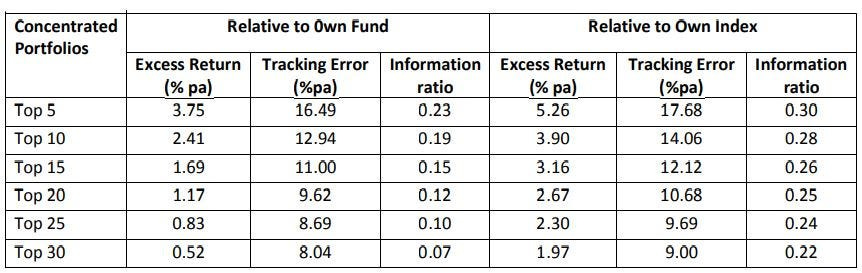

The table below shows different-sized portfolios.

The top 5, top 10 and so on relate to the hand-selected stock each fund manager had the most confidence in.

It also shows how each pool of stocks performed relative to their entire fund and the index.

The “excess return” of the “top 5” conviction-weighted portfolio was 3.75%, which means it made 3.75% more than the manager’s own fund.

The “top 5” again made a 5.26% excess return compared to the general index.

As you go down the chart and the stocks get less concentrated, the performance continues to decline.

The “tracking error” is just fancy for volatility, which is higher the more concentrated the stocks.

So you take the excess return. You then divide it by the tracking error, which gives you the “information ratio”, the risk-adjusted return (similar to a Sharpe ratio).

The higher the “information ratio” figure, the better the stock’s performance relative to risk.

The table shows how well the fund managers’ confidence in their investment choices paid off.

Concentration was the winner — every time.

.jpg){kind=link}

Final thoughts

Kevin O’Leary made a lousy investment in the now defunct crypto exchange FTX, losing about $9.7 million after the founder, Sam Bankrupt Fried, ran off with the money.

It’s an example of where diversification saved O’Leary.

But it digs into a more profound question.

Does diversification protect you against the unknowns, and if it’s unknown, do you have any right to invest and expect a positive outcome?

“Diversifying in practice makes very little sense to someone who knows what they’re doing.

Diversification is a protection against ignorance.

If you want to ensure nothing bad happens to you relative to the market, there’s nothing wrong with that for someone who feels they don’t know how to analyse businesses.

If you know how to value and analyse businesses, it’s crazy to own 40 stocks.

Putting money in number 30 or 35 on your list of attractiveness and foregoing putting more money into number one just strikes Charlie and me as madness”.

It all ultimately comes down to who you are.

If you’re unwilling to read up on individual companies regularly, investing in an ETF, Mutual fund, or Index or spreading your investments out will protect you against a lack of knowledge.

Buffett says the “know-something investor” who enjoys staying up to date with their investments should leverage their knowledge to achieve above-market returns.

It’s an approach I agree with.