Why I’ve Moved Most of My Crypto in SUI.

The macro influences almost no one is noticing.

Today’s newsletter was originally sent to paying subscribers back in November 2025. Since then, there’s been a wave of new readers coming in from TikTok and Instagram, so I wanted to reshare this piece to reinforce my stance on the asset I cover in this blog.

Volatility is the price you pay for exponential upside. Too many people at times like this decide to be tourists and step away, only to return when prices are climbing. The crazy upside is only possible in moments like this.

If you want to support our work and get closer to the community and how we’re navigating the market, consider upgrading.

The membership is designed to pay for itself over time. You get access to a private daily chat, monthly group calls, NFT giveaways, live streams, content shout-outs, and deeply researched insights without the usual jargon.

Hope you enjoy the blog.

As famous investor Peter Lynch once said:

“Far more money has been lost by investors preparing for corrections or trying to anticipate corrections than has been lost in corrections themselves.”

I’m reading a ton of theories about where this market is headed, and most of them drift further from reality than a drunk pigeon.

Last August, I got very vocal about a new blockchain called SUI, which was showing early signs of gaining mindshare on the timeline and outperforming most of the top 20 coins in price, and at the time, going toe to toe with Solana’s resurrection from $8 lows.

Adeniyi Abiodun, former Head of Research and Development for Facebook’s Libra project and now one of the five Co-Founders of SUI, explained the project's vision.

“Our Vision for Sui is to build a global coordination layer for intelligent assets, going beyond traditional blockchains. We’re creating a decentralised web stack that supports everything from smart contracts to decentralised storage with Warus, a global storage layer that is more distributed and cost-effective than AWS (cloud storage). This infrastructure will underpin a wide range of applications, offering unprecedented security and decentralisation.”

So it’s an infrastructure play designed to onboard the entire Web2 world onto Web3 seamlessly.

This matters because companies like Netflix, Apple, and Disney each burn through about $500 million a year on cloud-storage fees, the kind of money that makes you wonder why the whole Web2 internet wouldn’t jump to SUI’s high-speed, cost-efficient blockchain.

Franklin Templeton and BlackRock are actively leveraging SUI for tokenisation, and SUI has also partnered with the parent company of TikTok, ByteDance, for Web3 gaming and SocialFi apps.

This is no Mickey Mouse operation.

The ex-Facebook team is extraordinary. The technology is mind-blowing, and when I heard that macro and finance expert Raoul Pal was on their advisory board, it sealed the deal for me as a final, but significant, safety signal.

There’s one fundamental truth about SUI that very few notice.

It’s newer and smaller, which means it can rise faster than larger assets. If one person is in the network and one joins, that’s a 100% increase. But if one joins a network of 50, it’s only 2%. You get the idea.

The same logic applies in reverse, too, because it’s newer and more speculative, it also tends to bleed the most during drawdowns.

The drawdowns have been a stomach punch that, if I’m brutally honest, I didn’t expect at this stage in the cycle, not just in crypto but across financial markets.

It may come down to a simple explanation everyone knows but barely anyone’s clocking: crypto folks still glued to the old four-year cycle, convinced it’s time to sell because they think a bear market’s around the corner.

Rekt co-founder Mando pointed out that sentiment is scraping the floor. You only need ten minutes on X to feel it.

The Fear and Greed Index is at its weakest since the FTX collapse and March’s “tariff tantrum.” It measures Bitcoin sentiment across six signals: volatility, trading volume, social activity, surveys, Bitcoin dominance, and Google Trends. It’s about as sharp as a surgeon’s scalpel when it comes to sentiment.

Folks may be selling purely because they think the four-year cycle is running out of road.

Mando says he doesn’t expect a deep drop, though the sideways chop could drag on longer than most people want to admit.

I think he’s right.

“I am bullish on Risk Assets. At the same time, I am slightly data-driven, and I am cognizant—and have been for a while—that this was the four-year cycle time, and my bet was that it was going to extend. That being said, I think 50% of the market thinks on a four-year cycle because a lot of the OG Bitcoiners think like that. And if they all believe it, then maybe the market does go through a bit of an extended dip here, and you have to respect that that’s what the market believes. I don’t think it will be deep, and I think it will be a buying period. I do think that the correlation to M2 will return pretty aggressively. In 2026, M2’s only going higher, so I’m a buyer.”

Macro Indicators

Liquidity has been the puppet master of the financial markets.

I’ve lost count of how many times I’ve seen that M2 chart Mando references lined up next to Bitcoin with its tidy 12-week lead. Bitcoin basically shadowed the money supply until recently.

Now sentiment has flipped bearish, even though global M2 is sitting at an all-time high.

Some people (including me) blamed the government shutdown and reduced spending. Others (not including me) insisted it was the end of the cycle.

The mistake is assuming rough economic conditions automatically mean falling asset prices. They don’t. Central bankers don’t wait for the house to burn down, so they pump liquidity the moment smoke appears.

As Mike Howell, the global liquidity maestro since the 1980s, has shown, asset prices move in lockstep with central bank balance sheets.

When those expand, asset prices follow.

“If you have an expanding Fed balance sheet and an expanding injection of capital, that’s a recipe for very strong global liquidity. The best time for asset prices is when economies are slow and sluggish, but policymakers are trying to stimulate them, and that’s what we’ve got.”

Right now, the Fed is cutting rates.

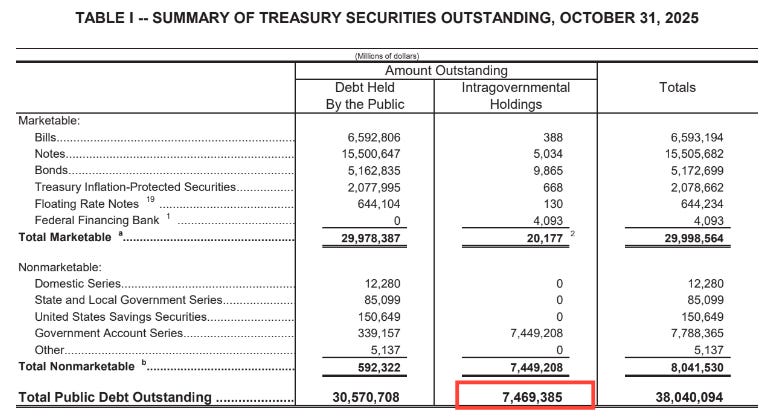

Once those rates drop to a more sensible level, they’ll have to refinance roughly $7.4 trillion in debt that’s coming due, the same can they kicked down the road during the 2020 refinancing wave.

The key point is simple: this debt has to be rolled over.

But when rates were near zero, most of it was refinanced with an average maturity of about 5.5 years, not the 3–5 years most people assume. There’s a growing view online that the liquidity story still holds, people are just getting the debt maturities wrong.

According to the Joint Economic Committee’s September update, as of Q3 2025, roughly 31% of U.S. publicly held marketable Treasury debt, about $9.39 trillion out of $30.3 trillion, will mature within the next 12 months.

So that takes us to September 2026.

That’s a massive cluster of near-term maturities. It ramps up the chances of a rollover because the Treasury has to refinance that wall of debt, and when they do, asset prices tend to float higher, and our magic internet money gets its ticket to the gates of Valhalla.

What this says to me is we need to extend our time horizon, not that the cycle is over.

As business cycle expert Julien Bittel says:

“Nothing new here. The Fed won’t start QE until they can roll over debts at more sustainable levels – meaning rates have to come down first. Also, when we talk about “moar cowbell,” we’re talking about global liquidity, which can come from the PBoC (for example), private credit creation, rate cuts, a weaker dollar, or lower bond yields. All of these ease financial conditions and support growth. Phase One: Rate cuts.Phase Two: Debts get monetized.”

It looks like there are some early signs of the Fed moving into panic mode.

The SRF, or Standing Repo Facility, is like the Fed’s emergency cash tap for banks.

When money gets tight, banks can borrow short-term cash using Treasuries as collateral. The issue is, they’re not using it, which worries the Fed. If banks avoid the SRF even when they need cash, it means there’s a deeper problem in the system, and that’s why nerves are rising.

Macro expert RP thinks something structurally will happen imminently.

“I think this week the Feds hand will be forced to tweak the plumbing to avoid a month-end and year-end funding crisis. Crypto is currently trading like a stressed funding vehicle reflecting the broken plumbing, while stocks are cushioned by buybacks and performance chasing for now, but risk a repeat of 2018/19 if not solved immediately. It’s clear the Fed are concerned, hence the meeting with the banks and NY Fed to understand why the SRF isn’t being tapped enough to resolve this. The fear from markets and the Fed is rising.”

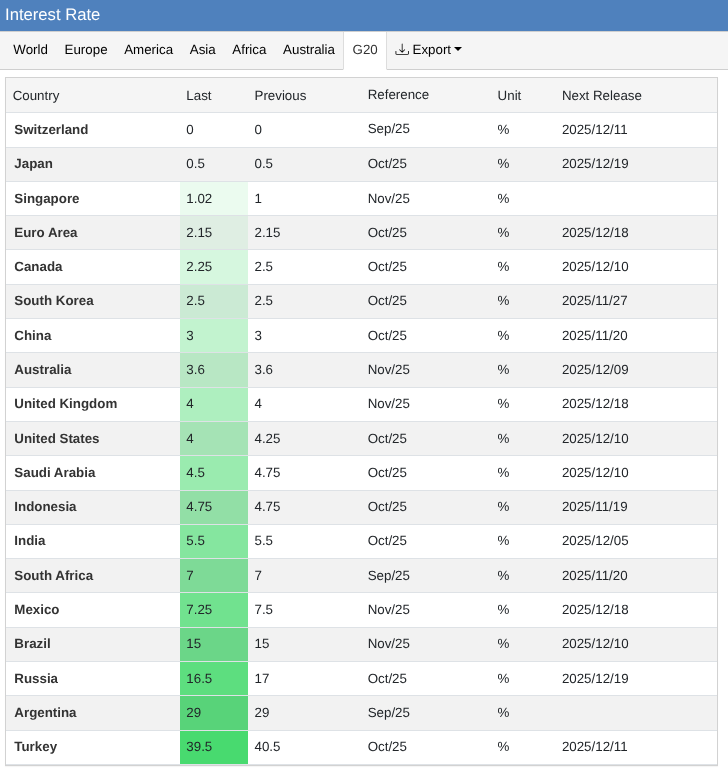

To loop back to Julien Bittell’s point about interest rates, we need to note that rates are dropping worldwide.

There are other factors besides the Fed.

Just look at the G-20, which comprises the world’s strongest economies: all but two are lowering rates. One is Japan, which has had record and returning inflation, and the other is Switzerland, which is already at a 0% interest rate.

The entire world is reducing rates, and people on the timeline are shitting their pants. Just think about it logically, if people have more money in their pocket, will they buy more or less crypto? Doesn’t take a rocket scientist to figure this stuff out.

The current movement, driven by basically the entire world, does not signal an overheated market or end-of-cycle behaviour, but rather the opposite.

The macro outlook is very positive.

Take the steady decline in oil prices, which is essentially a tax on the entire system.

When oil is high, it costs more to move goods, produce goods, and live day to day. That drains money from businesses and consumers, leaving less to invest, so assets like crypto and stocks stagnate or fall faster than a broken elevator.

When oil prices drop, it’s like giving the world a giant fucking pay rise.

We know our magical internet money is just a product of financial conditions and people having more money in their skyrocket for discretionary spending.

Costs ease, spending picks up, and central banks face less pressure to keep rates high, freeing up liquidity that flows back into markets and lifts risk assets.

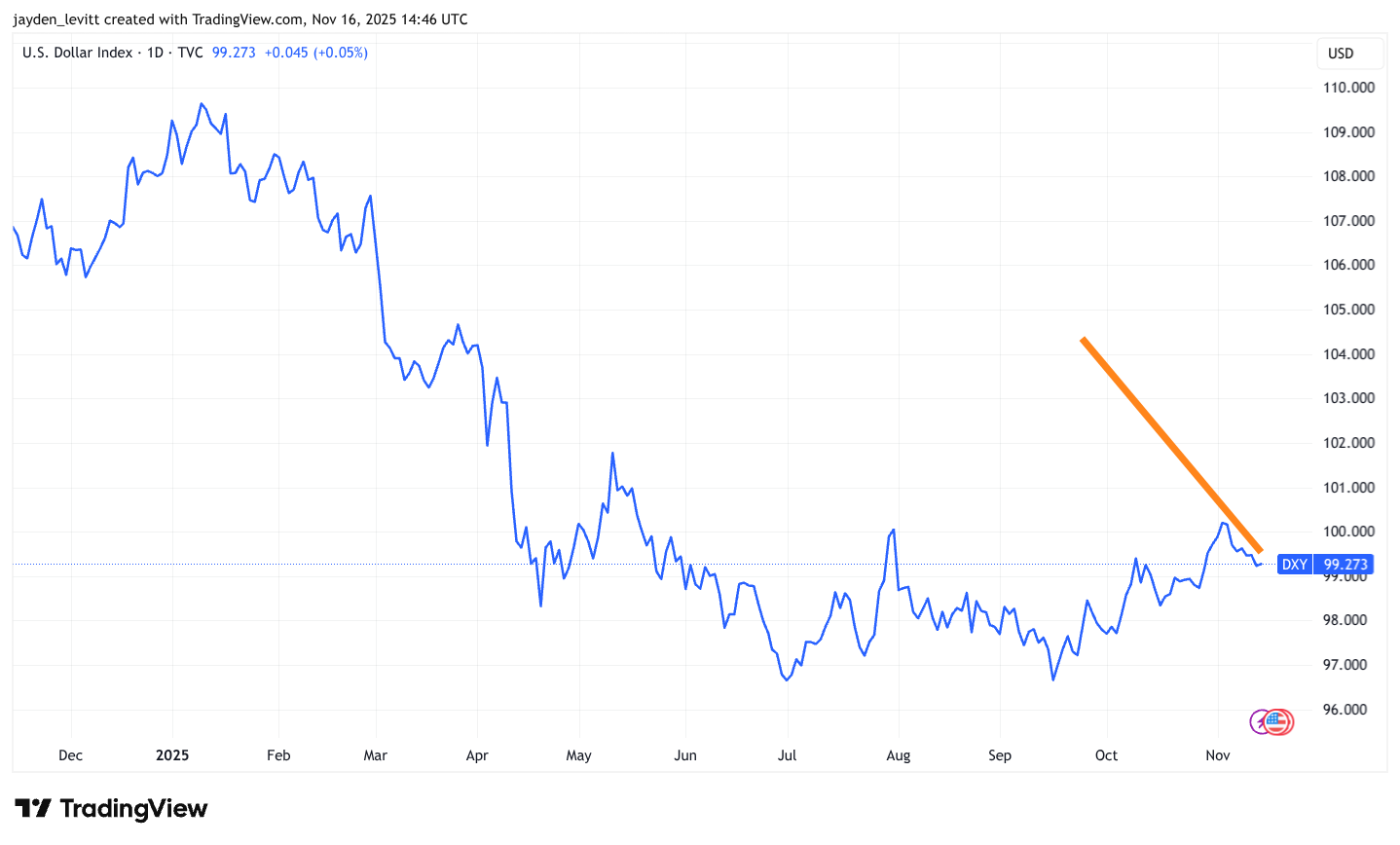

The dollar’s been quietly losing strength, and that’s a good thing.

Most of the world owes money in dollars. So when the dollar pumps, those debts get harder to repay. Countries need more of their own currency to buy the same number of dollars. That drains liquidity and tightens conditions, as we saw around Jan/Feb, right after Trump took office.

It appeared he was using a strong dollar as a stick to beat foreign leaders with during negotiations around the tariffs.

When the dollar softens, the pressure eases like letting a bit of air out of an overinflated tyre because there’s less crowding out of spending. But it also meant that China could print a shit ton of money without destabilising their local currency. And they did.

In short, a weaker dollar means stronger markets, and that’s exactly what we’re getting.

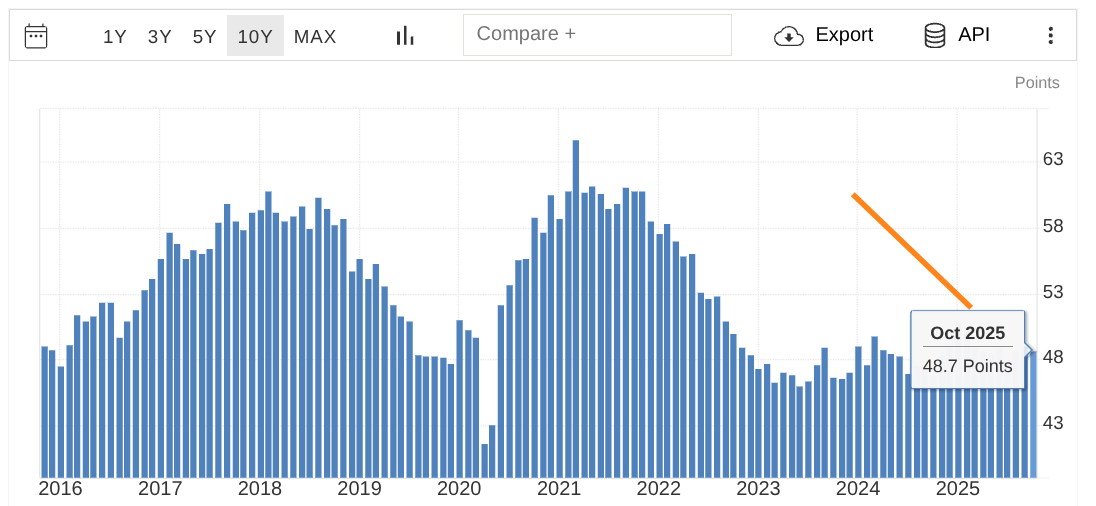

The ISM (Institute for Supply Management)

I share this data point often because I think it’s the bellwether for everything.

It’s the only thing I can think of that isn’t mid-curve nonsense or a misleading signal.

The ISM, specifically the PMI (Purchasing Managers’ Index) headline figure, is basically the economy’s pulse check.

It tracks the health of US manufacturing and services, and it’s one of the clearest signals of what’s coming next for liquidity and markets.

When the PMI runs hot, business activity surges, inflationary pressure builds, and central banks tighten the screws with higher rates. Liquidity dries up, and risk assets like crypto usually take the hit.

When the PMI cools, the opposite happens. Growth slows, central banks ease off, and liquidity flows back in, giving crypto, stocks, and other risk assets a fresh breath of oxygen.

In short:

High PMI = overheated economy

Low PMI = cooler economy

Right now, PMI has bottomed.

A score below 50 means cooling conditions, and anything around 60 signals overheating.

We’re far from the mania phase. We’re nowhere near the chaos of paying $500 in ETH gas fees like it’s confetti.

At 48.7, the reading shows we’ve bottomed, but it oscillates like a heart-rate monitor, and the next move looks to be up.

Again, you don’t need to be a brain surgeon to guess where the next move might be, considering the entire world is easing financial conditions.

Final Thoughts.

That’s why I’ve moved most of my crypto into SUI (my PNKSTR and NFTS haven’t moved).

I’m playing the multi-cycle game because these chances only show up every four years.

Last cycle, it was Solana. Four years prior, it was Ethereum as the anointed one. Both took 90% drawdowns on the chin. So SUI’s current correction isn’t fun, but it’s tame in comparison, and it says nothing about the quality of the asset.

Funnily enough, when I was speaking to Bren, an expert in technical analysis, he said if you saw those drawdowns in a stock, you’d assume the company was dead. He’s right. It really comes down to not applying old frameworks to a new set of rules.

Bitcoin has always experienced at least 5 brutal 30%+ drawdowns each cycle, and solid altcoins often drop by 60%+ in the process. As crazy as it sounds, it is actually completely normal.

I’ve seen this movie before. I held through ETH crashing to $80 after the ICO boom, Solana dropping from $247 to $8, and my NFT portfolio swinging from $1.4 million to $25k lows.

Now it’s SUI’s turn.

Nothing has fundamentally changed. There’s still a low float with only 37% of tokens on the market, so significant supply friction, and the market cap sits around $6 billion, with little buy pressure required for price gains.

The punchline is that the debt needs to be rolled over, but the Biden administration extended the maturity of the debts presumably to lock in the 0% rates for a longer period.

The bigger picture is extremely bullish.

The structural issues in the market might actually accelerate the Fed stepping in and tweaking the plumbing, as Raoul mentioned.

We’ve got $7.4 trillion in debt rolling over in the next 10 months, interest rates set to fall across 95% of central banks globally, oil prices retreating, the dollar index sliding (which adds liquidity), and the ISM already bottoming out and waiting for a rebound.

And for those saying, “But Jay, what about the AI bubble?”, people, including me, have been calling tech stocks a bubble since 2008.

Warren Buffett’s Berkshire Hathaway just dropped $4.9 billion into Google’s AI promise. He’s a value investor to the core, so either it’s a bubble or it’s undervalued. It can’t be both.

My take? We go much higher after some short-term pain.

Batten down the hatches, add where you can. Touch some grass. Kiss your dog on the fucking head.

Whatever keeps you sane, because in the end, we win.

If this blog gave you any value, a quick share goes a long way. It’s how Carrot Lane grows and how more people get real insight instead of noise. Appreciate you.

Great article

I’ve been buying SUI everyday in 2026